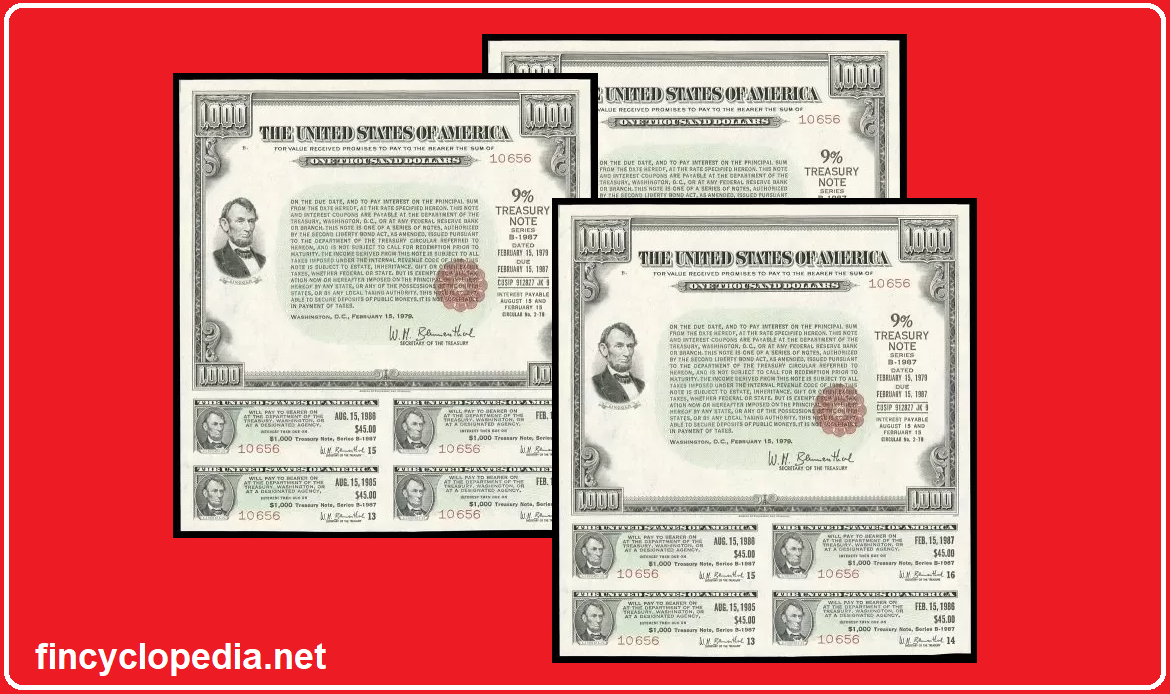

From the perspective of an issuer, a fixed-income security is a financial obligation for payment of a specific amount of money, being the fixed interest payment, at specific future dates (and over a span of time covering the security’s maturity or lifetime). At maturity, the issuer also repays the principal amount (the stated face value of the security at the time of issuance). Issuers of fixed-income securities may virtually take the form of any entity including a government agency, a local government entity, a corporation, and a supranational body (e.g., the World Bank).

In general, fixed-income securities have two basic types/ arrangements: debt obligations and preferred stock. Under the former arrangement, an issuer is a plain borrower (it borrows funds from holders of these securities, i.e., the investors). In which case, the issuer makes payment to holders at the specified dates, consisting of interest amounts and partial repayment of the amount borrowed. Examples of debt-obligation fixed-income securities include bonds, notes, mortgage backed securities (MBSs) and asset-backed securities (ABSs).

On the other hands, preferred stock constitute a hybrid mixture of debt obligation and ownership interest. Holders receive payment in the form of dividends (distributed profits, contractually fixed for holders of preferred stock) and repayment of a fixed amount, on specific intervals, to retire the debt obligation.